We profit from it, we fear it, and we find it impossibly hard to quantify… risk.

While not the sexiest of industries, insurance can be a life-saving protector, pooling everyone’s premiums to safeguard against some of our greatest, most unexpected losses.

One of the most profitable in the world, the insurance industry exceeded $1.2 trillion in annual revenue since 2011 in the U.S. alone.

But risk is becoming predictable. And insurance is getting disrupted fast.

By 2025, we’ll be living in a trillion-sensor economy, projected to generate bronto-bytes (1000 trillion trillion) of data, as explained by TSensors Summit co-founder Janusz Bryzek. And as we enter a world where everything is measured all the time, we’ll start to transition from protecting against damages to preventing them in the first place.

But what happens to health insurance when Big Brother is always watching? Do rates go up when you sneak a cigarette? Do they go down when you eat your vegetables?

And what happens to auto insurance when most cars are autonomous? Or life insurance when the human lifespan doubles?

For that matter, what happens to insurance brokers when blockchain makes them irrelevant?

In this blog, I’ll be discussing four key transformations:

- Sensors and AI replacing your traditional broker

- Blockchain revolution

- The ecosystem approach

- IoT and insurance connectivity

Let's dive in.

Artificial Intelligence and the Trillion-Sensor Economy

As IoT sensors continue to proliferate across every context — from smart infrastructure to millions of connected home devices to medicine — smart environments will allow us to ask any question, anytime, anywhere.

And as I often explain, once your AI technology has access to this treasure trove of ubiquitous sensor data in real time, it will be the quality of your questions that make or break your business.

But perhaps the most exciting insurance application of AI’s convergence with sensors is in healthcare.

Tremendous advances in genetic screening are empowering us with predictive knowledge about our long-term health risks.

Leading the charge in genome sequencing, Illumina predicts that in a matter of years, decoding the full human genome will drop to $100, taking merely one hour to complete. Other companies are racing to get you sequences faster and cheaper.

Adopting an ecosystem approach, incumbent insurers and insurtech firms will soon be able to collaborate to provide risk-minimizing services in the health sector.

Using sensor data and AI-driven personalized recommendations, insurance partnerships could keep consumers healthy, dramatically reducing the cost of healthcare.

Some fear that information asymmetry will allow consumers to learn of their health risks and leave insurers in the dark. However, both parties could benefit if insurers become part of the screening process.

A remarkable example of this is Gilad Meiri’s company, Neura AI. Aiming to predict health patterns, Neura has developed machine learning algorithms that analyze data from all of a user’s connected devices (sometimes from up to 54 apps!).

Neura predicts a user’s behavior and draws staggering insights about consumers’ health risks. Meiri soon began selling his personal risk assessment tool to insurers, who could then help insured customers mitigate long-term health risks.

But artificial intelligence will impact far more than just health insurance.

In October of 2016, a claim was submitted to Lemonade, the world’s first peer-to-peer insurance company. Rather than being processed by a human, every step in this claim resolution chain — from initial triage through fraud mitigation through final payment — was handled by an AI.

This transaction marks the first time an Artificial Intelligence has processed an insurance claim. And it won’t be the last. A traditional human-processed claim takes 40 days to pay out. In Lemonade’s case, payment was transferred within three seconds.

However, Lemonade’s achievement only marks a starting point. Over the course of the next decade, nearly every facet of the insurance industry will undergo a similarly massive transformation.

New business models like peer-to-peer insurance are replacing traditional brokerage relationships, while AI and blockchain pairings significantly reduce the layers of bureaucracy required (with each layer getting a cut) for traditional insurance.

Consider Juniper, a startup that scrapes social media to build your risk assessment, subsequently asking you 12 questions via an iPhone app. Geared with advanced analytics, the platform can generate a million-dollar life insurance policy, approved in less than five minutes.

But what’s keeping all your data from unwanted hands?

Blockchain Building Trust

Current distrust in centralized financial services has led to staggering rates of underinsurance. Add to this fear of poor data and privacy protection, particularly in the wake of 2017’s widespread cybercriminal hacks.

Enabling secure storage and transfer of personal data, blockchain holds remarkable promise against the fraudulent activity that often plagues insurance firms.

As explained by Symbiont’s President Caitlyn Long, “The centralized database model of insurance companies and other organizations is becoming redundant.” Developing blockchain-based solutions for capital markets, Symbiont develops smart contracts to execute payments with little to no human involvement.

But distributed ledger technology (DLT) is enabling far more than just smart contracts.

Also targeting insurance is Tradle, leveraging blockchain for its proclaimed goal of “building a trust provisioning network.” Built around “know-your-customer” (KYC) data, Tradle aims to verify KYC data so that it can be securely forwarded to other firms without any further verification.

By requiring a certain number of parties to reuse pre-verified data, the platform makes your data much less vulnerable to hacking and allows you to keep it on a personal device. Only its verification — let’s say of a transaction or medical exam — is registered in the blockchain.

As insurance data grow increasingly decentralized, key insurance players will experience more and more pressure to adopt an ecosystem approach.

The Ecosystem Approach

Just as exponential technologies converge to provide new services, exponential businesses must combine the strengths of different sectors to expand traditional product lines.

By partnering with platform-based insurtech firms, forward-thinking insurers will no longer serve only as reactive policy-providers, but provide risk-mitigating services as well.

Especially as digital technologies demonetize security services — think autonomous vehicles — insurers must create new value chains and span more product categories.

For instance, France’s multinational AXA recently partnered with Alibaba and Ant Financial Services to sell a varied range of insurance products on Alibaba’s global e-commerce platform at the click of a button.

Building another ecosystem, Alibaba has also collaborated with Ping An Insurance and Tencent to create ZhongAn Online Property and Casualty Insurance — China’s first Internet-only insurer, offering over 300 products. Now with a multibillion-dollar valuation, Zhong An has generated about half its business from selling shipping return insurance to Alibaba consumers.

But it doesn’t stop there. Insurers that participate in digital ecosystems can now sell risk-mitigating services that prevent damage before it occurs.

Imagine a corporate manufacturer whose sensors collect data on environmental factors affecting crop yield in an agricultural community. With the backing of investors and advanced risk analytics, such a manufacturer could sell crop insurance to farmers. By implementing an automated, AI-driven UI, they could automatically make payments when sensors detect weather damage to crops.

Now let’s apply this concept to your house, your car, your health insurance.

What’s stopping insurers from partnering with third-party IoT platforms to predict fires, collisions, chronic heart disease—and then empowering the consumer with preventive services?

This brings us to the powerful field of IoT.

Internet of Things and Insurance Connectivity

Leap ahead a few years. With a centralized hub like Echo, your smart home protects itself with a network of sensors. While gone, you’ve left on a gas burner and your Internet-connected stove notifies you via a home app.

Better yet, home sensors monitoring heat and humidity levels run this data through an AI, which then remotely controls heating, humidity levels, and other connected devices based on historical data patterns and fire risk factors.

Several firms are already working toward this reality.

AXA plans to one day cooperate with a centralized home hub whereby remote monitoring will collect data for future analysis and detect abnormalities.

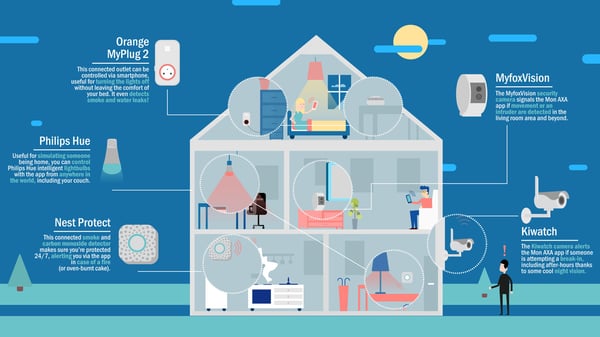

With remote monitoring and app-centralized control for users, MonAXA is aimed at customizing insurance bundles. These would reflect exact security features embedded in smart homes.

MonAXA connects homes to homeowners’ smartphones via IoT. Source: MonAXA

Wouldn’t you prefer not to have to rely on insurance after a burglary? With digital ecosystems, insurers may soon prevent break-ins from the start.

By gathering sensor data from third parties on neighborhood conditions, historical theft data, suspicious activity and other risk factors, an insurtech firm might automatically put your smart home on high alert, activating alarms and specialized locks in advance of an attack.

Insurance policy premiums are predicted to vastly reduce with lessened likelihood of insured losses. But insurers moving into preventive insurtech will likely turn a profit from other areas of their business. PricewaterhouseCoopers predicts that the connected home market will reach $149 billion USD by 2020.

Let’s look at car insurance.

Car insurance premiums are currently calculated according to the driver and traits of the car. But as more autonomous vehicles take to the roads, not only does liability shift to manufacturers and software engineers, but the risk of collision falls dramatically.

But let’s take this a step further.

In a future of autonomous cars, you will no longer own your car, instead subscribing to Transport as a Service (TaaS) and giving up the purchase of automotive insurance altogether.

This paradigm shift has already begun with Waymo, which automatically provides passengers with insurance every time they step into a Waymo vehicle.

And with the rise of smart traffic systems, sensor-embedded roads, and skyrocketing autonomous vehicle technology, the risks involved in transit only continue to plummet.

Final Thoughts

Insurtech firms are hitting the market fast. IoT, autonomous vehicles and genetic screening are rapidly making us invulnerable to risk. And AI-driven services are quickly pushing conventional insurers out of the market.

In 2017, there were 3.8 billion digitally connected people on the planet.

By 2024, roll-out of 5G on the ground, as well as OneWeb and Starlink in orbit are bringing 4.2 billion new consumers to the web — most of whom will need insurance.

Yet, because of the changes afoot in the industry, none of them will buy policies from a human broker.

While today’s largest insurance companies continue to ignore this fact at their peril (and this segment of the market), thousands of entrepreneurs see it more clearly: as one of the largest opportunities ahead.

Join Me

(1) A360 Executive Mastermind: This is the sort of conversation I explore at my Executive Mastermind group called Abundance 360. The program is highly selective, for 360 abundance- and exponentially minded CEOs (running $10M to $10B companies). If you’d like to be considered, apply here.

Share this with your friends, especially if they are interested in any of the areas outlined above.

(2) Abundance-Digital Online Community: I’ve also created a Digital/Online community of bold, abundance-minded entrepreneurs called Abundance-Digital. Abundance-Digital is my ‘onramp’ for exponential entrepreneurs – those who want to get involved and play at a higher level. Click here to learn more.

Written by: Peter H. Diamandis

Abundance Insider: October 12th, 2018

Abundance Insider: October 19th, 2018